Alice in Argentina

Where up is down and down is up...

“I wonder if I shall fall right through the earth! How funny it’ll seem to come out among the people that walk with their heads downwards.”

~ Lewis Carroll, Alice’s Adventures in Wonderland (1865)

Joel Bowman with today’s Note From the End of the World: Buenos Aires, Argentina...

It is no secret, dear reader, we live in a downside-up world. Perhaps you’ve noticed?

Among the northern, “developed” countries, trade barriers go up... economic growth is revised down... and inflation is beginning to rear its hideous head...

Leaders on both sides of the Atlantic, with feet in the clouds and sand in their heads, appear hopelessly lost, seemingly making the script up as they go.

Here in the developing south, meanwhile, trade barriers are coming down... economic growth is revised higher... and dreaded inflation has fallen to its lowest level this decade.

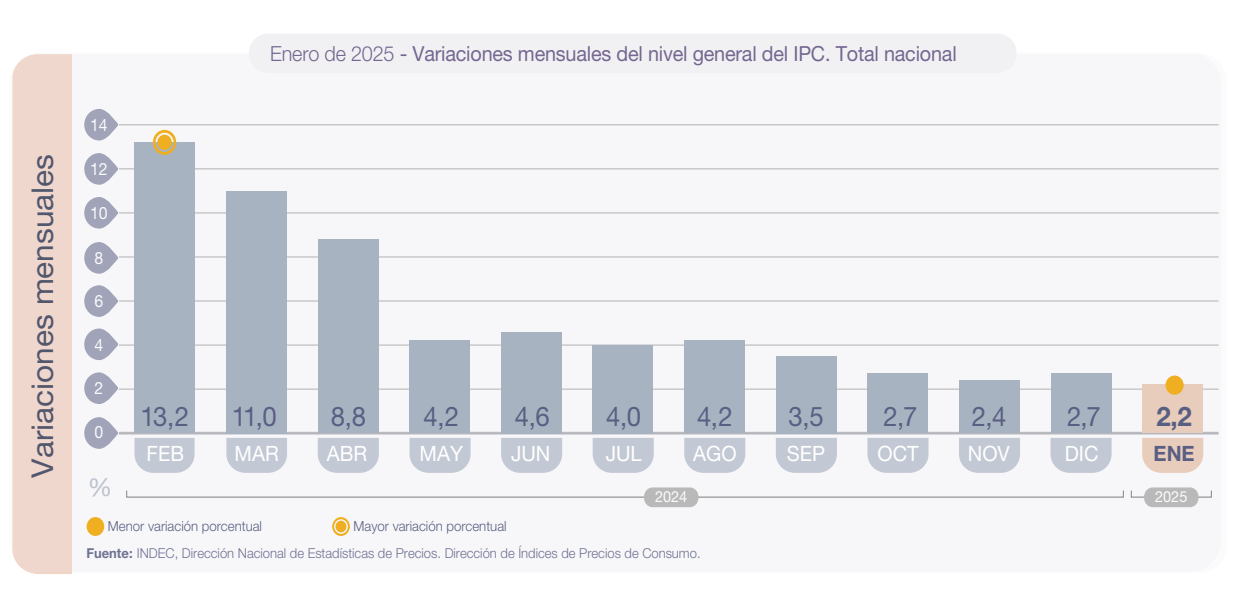

Witness the monthly inflation figures over the past year, from Argentina’s National Institute of Statistics (INDEC):

A Tale of Two Hemispheres

According to the central bank's market expectations survey, released yesterday, Argentine analysts project inflation will end the year at an annual rate of 23.3%. That’s down from nearly ~300% just 15 months ago... when stores didn’t bother pricing items on the (mostly empty) shelves and the right hand side of restaurant menus was left eerily blank.

Quite a turnaround, you’ll surely agree.

As for economic growth, that too is shaping up to be a “Tale of Two Hemispheres.” In the US, the Big Banks are adjusting southward their GDP estimates for the year. From GuruFocus:

Goldman Sachs just dropped a major warning on the US economy, cutting its 2025 GDP forecast to 1.7% from 2.4% as Trump's tariff policies start to take shape. Morgan Stanley followed suit, slashing its estimate to 1.5%.

Both firms now see inflation running hotter, with Goldman predicting the Fed's preferred inflation gauge will end the year at 3%, while Morgan Stanley expects 2.7%.

The culprit? A steep 10-percentage-point jump in the average US tariff rate—five times higher than the peak under Trump's first term. Analysts say the ripple effects could be brutal: higher consumer prices, tighter financial conditions, and stalled business investment.

Meantime, at this End of the World, “among the people that [typically] walk with their heads downwards,” revisions are made in the opposite direction.

Forecasts for GDP growth this year range from 4.5% (from the central bank) to 5% (the World Bank), representing between a 7.3 to 7.8 percentage point turnaround from last year’s 2.8% annual decline.

As usual, there’s always more to the story... and when it comes to the government’s (any government’s) economic data, the legerdemain flows forth like bad advice from a Davos lapdancer. All is not quite as it seems, in other words. It’s worse.

To understand why the GDP story is not the whole story (and far from it), we need to take a look under the hood of this rotten government metric, one which bewilders and misdirects far more than it edifies. We intend to make several points over the next few Notes, each of which will profit from a better understanding of this most mystifying metric. Ergo, a brief refresher...

The GDP Myth

According to our trusty Encyclopedia Britannica, gross domestic product (GDP) is defined as the “total market value of the goods and services produced by a country’s economy during a specified period of time.”

Ordinarily, we hear GDP expressed as a percentage, that is, a rate of growth, either positive or negative. Ask any man on the street and he will quote the latest figure to back up his bullish or bearish sentiment, to help him decide whether to buy or sell, to take a holiday... or look for a second job.

The feds, meanwhile, cite the very same figure to help justify their own course of action; whether the economy needs to be “stimulated” or “cooled;” whether to slash or hike rates; to merely inflate... or to hyperinflate.

A lot rides on this magic number, in other words, even as it’s predicted, prognosticated, conjectured, aggregated, tortured, averaged, announced, revised and re-revised ad nauseam each and every quarter.

Even so, most people tend to think of GDP as some kind of definitive reading, spat out of a complex, high-powered machine, which testifies reliably, irrefutably, quantitatively as to the overall health and vitality of something called “the economy.”

Ah, but what, exactly, is this thing we are measuring, this “economy”?

As Frank Shostak, adjunct scholar at the Mises Institute, once put it:

“The GDP framework gives the impression that it is not the activities of individuals that produce goods and services, but something else outside these activities called the ‘economy.’ However, at no stage does the so-called ‘economy’ have a life of its own independent of individuals. The so-called economy is a metaphor—it doesn't exist.”

We’ll come back to the metaphor... ahem, the “economy”... in a moment. First, let us consider briefly the computation of the GDP measurement itself. There are three primary methodologies used to calculate GDP:

The expenditure method

The income method and

The value added method

The Cost of Government

Theoretically, all three methods should produce the same result although, in practice, this almost never happens. For instance, when there is a large surge in public spending, such as the never-ending Niagara of pandemic relief packages, stimmie programs, loan and grant hustles, payment protection schemes, climate boondoggles, equity subsidies and assorted other free-for-all lolly scrambles, one would expect significant GDP “growth” to register in the expenditure method.

Roughly speaking, this method calculates the “size” of an economy by totaling its expenditures, minus imports. The equation looks like this:

GDP = private consumption + gross investment + government spending + (exports − imports). Or, GDP = C + I + G + (X − M).

The adroit reader will notice immediately the prestidigitation afoot, that “government spending” is counted as a net positive, a “+.” Here’s how the Commerce Department’s Bureau of Economic Analysis explains it...

Gross domestic product (GDP), or value added, is the value of the goods and services produced by the nation’s economy less the value of the goods and services used up in production.

So far, so good. Until (emphasis ours)...

GDP is also equal to the sum of personal consumption expenditures, gross private domestic investment, net exports of goods and services, and government consumption expenditures and gross investment.

As the Department of Government Efficiency (DOGE) has lately exposed, a country that spends money it does not have on programs it does not need (that the majority of its citizens do not even know exist) is hardly embarked on the road to riches.

Not only are the vast majority of government programs unsustainable, mendacious and distortive scams, measuring them as a “+” under the expenditure GDP calculation separates further the reality individuals experience in their workaday lives from the GDP fantasy their governments serve up to them.

For one thing, this methodology ignores the fact that government spending is not true production at all because it is debt financed. (Imagine maxing out your credit cards to load up on meme coins and counting your “investment” as a net positive in your Gross Household Product (GHP)).

Government spending, ultimately, should really only be government spending less government borrowing.

Austrian Alternatives

Murray Rothbard, a key figure in the Austrian School of Economics, sought to address this “oversight” when he proposed his twin alternative measures: Gross Private Product (GPP) and Private Product Remaining (PPR).

Rothbard defined the former as “gross national product less income originating in government and government enterprises.” PPR is GPP less the higher of government expenditures and tax revenues plus interest received. Rothbard argued that because government output is “financed coercively” (i.e., by taxation), it is therefore unclear what - if any - market value may be ascribed to the end product.

Simply put, both Rothbard’s measures place government “production” where it belongs: in the “opportunity cost” pile.

If free market participants did not deem it worth their while to buy something in the first place, why should it be considered a net positive when the government confiscates their money (and/or that of their unborn children) to purchase it on their behalf? The case may be brought against practically every government expenditure which, even if it was allocated to something everyone agreed they wanted (decent roads, for example), nevertheless crowds out competition from private enterprises to provide that very same good or service.

In the end, GDP as a measurement can no more calculate the health of an economy than it can give you a foot massage or run a four-minute mile.

However it is measured, true economic progress is forged not in the crucibles of debt or coercion, but from the honest toil of individuals seeking to better their own lot, unhindered by the government’s long, strangulating reach. And if a positive GDP figure factors in a massive expansion in government expenditure, the only thing ultimately being measured is the rate at which the country is going to rack and ruin.

So where does that leave us, dear reader? And what does it reveal about the trajectory of economic growth, from one End of the World to the other?

Is down really up, and up really down? Are we really through the looking glass? Or have we merely fallen right through the earth?

Stay tuned for more Notes From the End of the World...

Cheers,

Joel Bowman

P.S. A special shoutout to our dear Notes Members; we’re ever grateful for your generous and ongoing support.

As mentioned in this space previously, Notes From the End of the World is an entirely independent, reader-supported publication (as in, we accept no advertising, bow to no boss, bend no knee).

We’re interested in free markets, free minds and free people…and we hope you are too!

So if you’re enjoying our work, and would like to help support the project, please consider joining our small but growing community of free-thinkers, deep readers and cheerful skeptics, here…

Excellent article Joel. Government "contribution" to GDP is a joke. It should be considered that the GDP gained from government spending has actually been negative and that should be a lesson to all the American people. Government is a cost not a growth of GDP. AND those in the stock market trying to gain savings should be aware that government expenditures have not been bringing greater growth to the economy, hence the reason for the current downtrend in stocks i.e. reality strikes every once in a while despite Wall Street propaganda campaigns and CFPlanners and that entire scheme.

As a friend who teaches the dismal science of Economics would say to his class as an example: "If the US were to produce missiles for Ukraine that would (hopefully) find their destination in Russia, you would have a net increase in GDP due to the manufacture of the munitions, followed by another net increase as those weapons are exported. Therefore, war is always a benefit to the economy!"

His example would demonstrate the upside-down nature of modern Economics, and show the uselessness of believing in government statistics.